The radio was playing softly in my car when I heard her voice cut through the static. A caller on KTSA’s afternoon talk segment about Social Security benefits said something that made me reach for my notepad on the passenger seat: “I work at a bank. I process other people’s transactions all day long. And I still can’t figure out why my son’s check came two days late last month and cost us $200 in overdraft fees.”

That was Rosalind Uribe, 50, a bank teller from San Antonio, Texas. I tracked down her contact through the station’s producer the following afternoon and called her that evening. She picked up on the second ring, and it was immediately clear she had been waiting to tell this story to someone who would actually write it down.

The Woman Behind the Counter

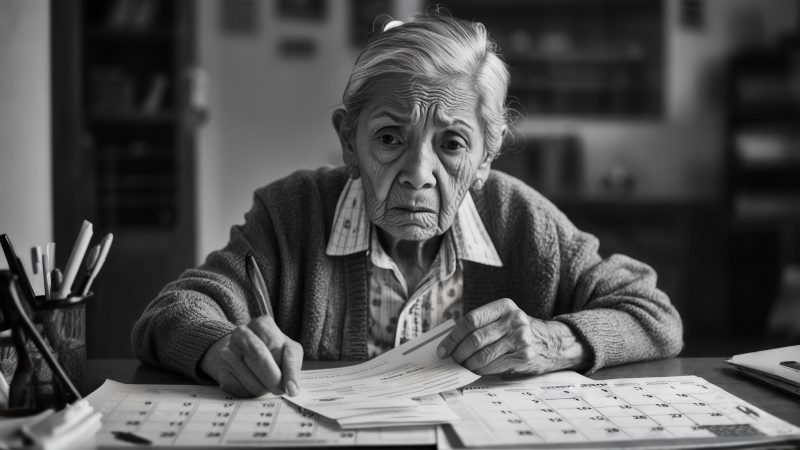

When I sat down with Rosalind Uribe at a coffee shop near her branch on Blanco Road two weeks later, she arrived with a folder. Inside: printed bank statements, a highlighted SSA payment calendar, and a stack of sticky notes. This was not a woman who let things go unexamined.

Rosalind has worked as a bank teller for nearly 14 years. She and her husband Marco earn a combined income that puts them comfortably above the median for San Antonio — she estimated roughly $118,000 together before taxes. By most measures, they are doing well. But their son Dominic, 9, has a complex neurological condition requiring round-the-clock specialized care. His in-home care provider alone costs approximately $1,840 per month. Dominic qualifies for Supplemental Security Income through the Social Security Administration, and that monthly payment — $967 in 2025 — had become a load-bearing piece of their budget.

On top of that, a medical emergency in the fall of 2023 left them with roughly $8,400 in credit card debt. Rosalind was managing payments on three cards simultaneously, each with a different due date. Every dollar of timing mattered.

When the COLA Arrived — and the Calendar Moved

Rosalind had heard about the 2025 Cost-of-Living Adjustment. She knew that SSA’s COLA for 2025 came in at 2.5 percent, nudging Dominic’s monthly SSI from $943 to $967. She was counting on that $24 bump to offset an increase in Dominic’s therapy co-pay that took effect the same month.

What she did not anticipate was what happened to the payment date. Because January 1, 2025 fell on a New Year’s Day holiday, SSA issued Dominic’s January payment on December 31, 2024 — one day early. The February payment then arrived on February 1 as scheduled. In Rosalind’s budget spreadsheet, those two payments looked like they had merged into one month, leaving January looking empty.

“I’m looking at my checking account on January 8th and I’m thinking — where is the deposit?” Rosalind told me, leaning forward over her coffee. “I know how direct deposit works. I set up hundreds of them at my branch. But I genuinely did not connect the dots that the December 31st deposit was the January payment.”

She had already scheduled two credit card payments and the caregiver’s weekly pay to pull from that account in early January. When the balance fell short, the overdraft fees hit in rapid succession. By January 10th, she had absorbed $200 in fees — nearly erasing the $24 COLA gain eight times over before the month was half done.

How SSI Payment Dates Actually Work — and Why They Shift

SSI payment rules are different from Social Security retirement benefits, and the distinction tripped up Rosalind in a way she found embarrassing in retrospect. Retirement and disability benefits (SSDI) are typically paid on Wednesdays based on the recipient’s birth date. SSI, by contrast, is paid on the first of every month — no birth date calculation involved.

When the first of the month lands on a weekend or federal holiday, according to SSA’s payment rules, the deposit is issued on the prior business day. That means December 31 for a January 1 holiday. The SSA does publish these adjusted dates in advance, but Rosalind told me she had never seen a notification come through her MySSA account about the calendar shift.

The Side Hustle That Couldn’t Plug the Gap Fast Enough

Rosalind described herself to me as someone who is always looking for ways to get ahead. She drives for a food delivery app on weekends. She sells handmade jewelry on a crafting marketplace. In the months after the January incident, she told me she had earned an extra $370 in February and $290 in March through her side work — just enough to start chipping away at the $8,400 credit card debt again after the overdraft fees had set her back.

“I hate standing still financially,” she said. “Even when things go sideways, I need to feel like I’m moving. That’s just who I am.”

But the January debacle exposed a vulnerability she had not fully reckoned with: even a high household income does not insulate you from cash flow problems when your expenses are both high and precisely timed. The caregiver’s pay cycle, the credit card due dates, and Dominic’s SSI payment were all synchronized in a way that left almost no buffer for a two-day calendar shift.

What Rosalind Knows Now That She Didn’t Then

By the time I spoke with her in March 2026, Rosalind had overhauled how she tracks Dominic’s payments. She set up a separate checking account specifically for SSI deposits and caregiver payments — a buffer account she does not use for credit card auto-pay. She checks the SSA payment calendar every October, when the following year’s schedule is released, and marks every adjusted date in her phone with a three-day advance alert.

“It sounds obvious now,” she admitted. “But when you’re working full-time, managing Dominic’s appointments, and running a side business on weekends, ‘check the SSA calendar in October’ is not the thing that rises to the top of your list.”

She also negotiated with one of her credit card issuers to shift her due date from the 8th of the month to the 15th — giving her payment window more breathing room relative to Dominic’s typical deposit date. That single change, she told me, reduced her financial anxiety measurably. The $8,400 debt is now down to approximately $5,900 as of this spring.

There is a particular frustration Rosalind carries that I found hard to shake after our conversation. She handles direct deposits professionally. She explains overdraft fee structures to customers at her bank window. And yet the system she navigates for her own son contains a layer of timing complexity that caught her — experienced, financially literate, high-earning — completely off guard.

That gap between financial knowledge and financial system transparency is not unique to Rosalind. But in her case, the cost of that gap landed with specific precision: $200 in fees, a setback on the debt she’s been grinding down for two and a half years, and a January that felt more like a step backward than the fresh start the COLA increase was supposed to deliver.

When I left her that afternoon, Rosalind was already pulling up her phone to show me the October reminder she’d pre-set for this coming fall. The notification read: “Check SSA payment calendar. Don’t trust January.”

Related: She Lost Her Husband at 32. Social Security Said She’d Have to Wait Until 60.

Related: She Lost $287 a Month in SNAP Benefits the Day Her Husband Stopped Working — Now She’s Drowning in Medical Debt

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply