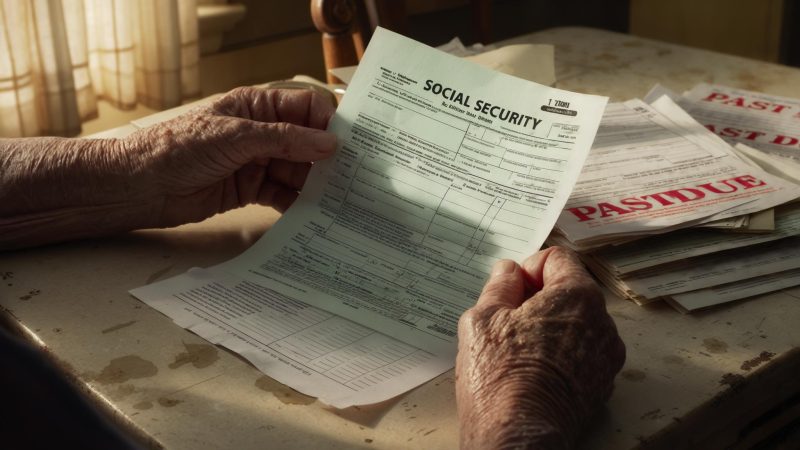

The folder was sitting right there on the kitchen table when I arrived — a manila envelope stuffed with SSA benefit estimates, a printed spreadsheet in 10-point font, and a highlighted printout of a news article about Social Security’s funding crisis. Bonnie Fitzgerald had been expecting me. She had been expecting this conversation for weeks, maybe longer, and she wanted to be ready for it.

I had been introduced to Bonnie by Pastor Elias Moreno at Crossroads Community Church in El Paso, Texas. He had mentioned her almost in passing after a Sunday service — a parishioner who was sharp, organized, and quietly unraveling over what she called “the math that stopped adding up.” He thought her story was worth telling. He was right.

A Plan That Looked Solid, From the Outside

When I sat down with Bonnie Fitzgerald at her kitchen table in late March 2026, the first thing she said was that she had done everything right. She said it plainly, without self-pity — a statement of fact, not a complaint. And by most measures, she had.

Bonnie, 59, is a registered nurse at a regional medical center in El Paso. She has worked in healthcare for 31 years, logged tens of thousands of hours, and over the past decade had built her household income into something that felt, for the first time, genuinely stable. She and her husband Marcus — who works in IT management — remarried five years ago, blending a family that now includes three adult and near-adult children between them. Their combined income had reached roughly $165,000 a year before a staffing restructuring at her hospital eliminated the overtime shifts that had become a quiet cornerstone of her financial plan.

“I was pulling in about $18,000 a year just in overtime,” she told me, spreading her hands flat on the table. “That sounds like a lot until you factor in what it was covering — the home equity line payment, the kids’ last tuition bills, the emergency fund I was trying to rebuild. When it stopped, I felt it immediately.”

The home repairs are not a minor inconvenience. Their house, built in 1987, needs foundation stabilization work and a full HVAC replacement. Two contractors have come out; both quoted figures close to $22,000. Bonnie has a folder for that too.

All of this — the overtime loss, the repair backlog, the blended family obligations — was already a pressure Bonnie was managing. Then she read about the Social Security insolvency projections. And then she read about the proposal to cap benefits.

The Insolvency Timeline She Could Not Ignore

Social Security’s trust fund is projected to become insolvent in roughly seven years. That is not a worst-case scenario — it is the current actuarial estimate. Under existing law, if the trust fund is depleted, the program would be required to cut benefits by approximately 24% across the board, paid from incoming payroll tax revenues alone. For someone like Bonnie, who is 59 and planning to claim benefits around age 66, that timeline is not abstract. It lands squarely in her retirement window.

Bonnie’s SSA benefit estimate, pulled from her My Social Security account, projects a monthly payment of approximately $2,480 at her full retirement age of 67, or roughly $2,190 if she claims at 65. A 24% cut would reduce those figures to $1,885 or $1,664, respectively. She had done the math herself, twice, on the spreadsheet in front of me.

“I kept thinking I was doing the calculation wrong,” she said. “So I did it again. I wasn’t doing it wrong.”

The $100,000 Cap Proposal — And Why It Complicates Everything

In late March 2026, a proposal from the nonpartisan Committee for a Responsible Federal Budget drew widespread attention. As reported by CBS News, the CRFB suggested limiting annual Social Security benefits to $100,000 for couples at full retirement age and $50,000 for single retirees — a structural change aimed at reducing the program’s long-term funding gap. According to the CRFB’s own analysis, capping benefits at those thresholds could save as much as $190 billion over a decade.

The proposal is framed as targeting the wealthiest beneficiaries — couples currently collecting more than $100,000 annually in combined Social Security payments. But the conversation it has opened is broader, touching on questions about benefit equity, means testing, and what the program is actually designed to do.

For Bonnie, the proposal landed differently than it might for someone a generation older. At 59, she is close enough to retirement to feel the policy debate as a personal threat, but not yet close enough to have locked in any benefits. She is, as she put it, “in the exact wrong position to absorb any of this.”

Running the Numbers She Was Not Ready to Run

Bonnie had always thought of Social Security as a foundation — not the whole structure, but the floor. Her 403(b) contributions, a modest brokerage account she started in her late 40s, and Marcus’s 401(k) were supposed to sit on top of that floor. The floor was supposed to be reliable.

What she described to me was not panic, exactly. It was the recalibration that happens when a long-held assumption is suddenly uncertain. She pulled up the comparison she had built:

The gap between the best and worst case in that table is more than $9,700 a year — roughly the equivalent of what Bonnie now spends annually on one of her children’s remaining college expenses. It is not a rounding error in a retirement budget.

“I’ve been a nurse for 31 years,” she told me, her voice steady. “I understand risk. I counsel patients about it every single day. But there’s something different about seeing it applied to your own life and realizing you don’t have a good answer.”

What She Is Doing — and What She Is Not Sure About

Bonnie has made some concrete moves since the news cycle around Social Security solvency intensified this spring. She increased her 403(b) contribution by three percentage points in January 2026, redirecting money that had been covering discretionary spending. She and Marcus have postponed the foundation repair until later in the year, hoping to accumulate more cash reserves first.

What she has not done — and says she is reluctant to do — is dramatically alter her expected retirement age based on proposals that have not become law. That hesitation is both understandable and, she acknowledged, potentially risky.

“I don’t want to make permanent decisions based on a proposal that might not pass,” she said. “But I also can’t pretend I didn’t read what I read. So I’m stuck in this middle place where I’m hedging without knowing what I’m hedging against.”

That middle place — between planning for a system that may change and refusing to abandon a plan built over decades — is where a lot of people in Bonnie’s position find themselves. She is neither wealthy enough to be unaffected by a benefit cut nor young enough to fully restructure her retirement strategy around the uncertainty.

A Conversation That Did Not End With Answers

I left Bonnie’s kitchen that afternoon with my notebook full and no tidy resolution to offer. The proposed $100,000 benefit cap, as Fortune reported, represents one possible path toward solvency — but even its proponents acknowledge it addresses only a portion of the long-term funding gap. And for someone like Bonnie, whose projected benefits fall nowhere near those thresholds, the cap is less a direct concern than a signal that the larger system is under pressure.

She walked me to the door and mentioned, almost as an afterthought, that she had been thinking about picking up per diem nursing shifts to replace some of the overtime income. Not because she wants to work more — she has been working full-time for 31 years — but because the math, as she now understood it, demanded more inputs.

The folder was still on the table when I left. I suspect it will still be there, updated, the next time someone sits down with Bonnie Fitzgerald to talk about what she has built and what she is afraid of losing.

What struck me most, driving back through El Paso that afternoon, was not the complexity of Social Security reform — it was how deeply personal a policy debate becomes when the person across the table has a spreadsheet, a highlighted article, and 31 years of work sitting on the line.

Leave a Reply