Roughly 70 percent of Americans who turn 65 today will need some form of long-term care at some point in their lives, according to the Administration for Community Living. Medicare, the federal health insurance program most people expect to carry that burden, covers almost none of the ongoing assisted living costs that consume tens of thousands of families each year. For Linda Chen-Ramirez, that gap stopped being a statistic about fourteen months ago when her phone rang and a billing coordinator at an assisted living facility in San Jose quoted her a monthly figure she hadn’t prepared for.

I met Linda on a Tuesday afternoon at a coffee shop near her office in downtown San Jose. She arrived in a blazer with a leather portfolio under her arm — the posture of someone who has trained herself to stay organized even when the underlying numbers refuse to cooperate. She is 58, works as a senior accountant at a mid-size tech firm, and has spent the better part of a decade rebuilding a financial life that a divorce at 49 very nearly dismantled. She ordered a black coffee and got straight to the point.

The Bill That Didn’t Match the Assumption

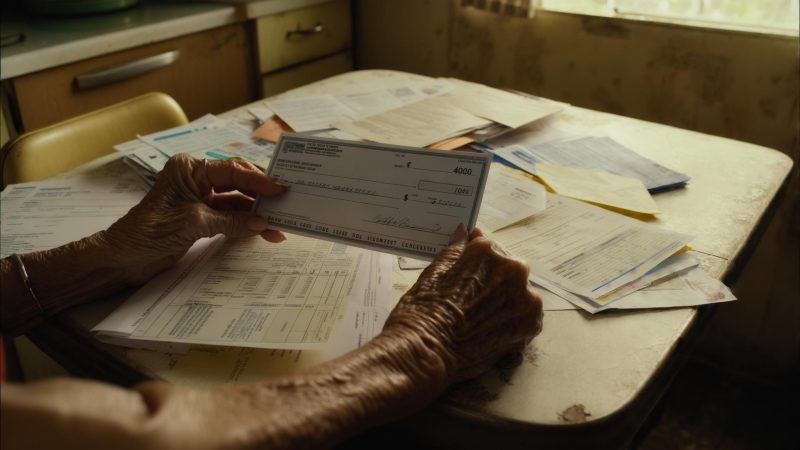

Linda’s mother, now 82, was diagnosed with moderate cognitive decline in early 2024. After several months of in-home support that became unmanageable, the family moved her into a memory care unit at an assisted living facility in San Jose’s Willow Glen neighborhood. The monthly cost: $6,800. Linda had assumed — as many adult children do — that Medicare would step in and absorb a meaningful portion of that expense.

It did not. According to Medicare.gov, the program covers skilled nursing facility care only under specific circumstances, and only for up to 100 days per benefit period following a qualifying hospital stay. Assisted living — the kind of residential memory care where Linda’s mother now lives — is not covered by Medicare at all. Custodial care, which includes help with bathing, dressing, and daily supervision, falls entirely outside Medicare’s scope.

Linda told me she had done research before placing her mother. She had read about Medicare benefits and believed the coverage was more comprehensive than it turned out to be. “I am an accountant,” she said, with a short, self-deprecating laugh. “Reading financial documents is literally my job. And I still missed this.” The distinction between skilled nursing and custodial care is written plainly in Medicare’s documentation, but it’s a distinction that doesn’t register until the invoice arrives.

The Squeeze Between Two Generations

What makes Linda’s situation particularly difficult to sit with is that the $6,800 monthly bill doesn’t exist in isolation. Her daughter, now 19, is finishing her first year at UC Santa Barbara. Linda is covering tuition and housing costs — approximately $35,000 annually — out of a combination of savings and current income. She told me she refused to let her daughter take out loans if she could avoid it, a decision that is equal parts love and guilt from a divorce that uprooted the family when her daughter was eight.

“I know what it feels like to have the financial rug pulled out from under you,” Linda said. “I wasn’t going to let that be her starting point in life.” That determination is admirable and, by her own admission, expensive. Between her mother’s care and her daughter’s tuition, Linda is absorbing roughly $116,000 in annual costs that sit outside her own household budget.

She still maxes out her 401k each year — $31,000 in 2026, including the over-50 catch-up contribution — and she is proud of that discipline. But she was 49 when her marriage ended and the settlement forced her to liquidate retirement assets she had spent two decades building. She estimates she lost roughly six years of compounding growth that she cannot fully replace by 67, even at her current savings rate.

What She Learned About Medicare’s Actual Boundaries

After the first invoice, Linda said she spent two weekends going through Medicare’s official coverage documentation with the same rigor she applies to corporate tax filings. What she found clarified the coverage structure — but didn’t make it easier to accept. Medicare Part A covers inpatient hospital stays, hospice care, and limited skilled nursing facility care. It does not cover room and board in an assisted living facility under any conditions.

Medicaid — the joint federal-state program distinct from Medicare — does cover long-term care for individuals who meet income and asset thresholds. Linda’s mother does not currently qualify. “She has some savings, a small pension, and the house hasn’t sold yet,” Linda explained. “By Medicaid’s asset rules, she has too much. But by actual living-in-San-Jose rules, it disappears fast.”

The Medicaid spend-down process — in which a person depletes assets to qualify — is something Linda has researched but hasn’t fully resolved. “I’m not there yet and I don’t want to think about it the wrong way,” she said carefully, clearly aware that any planning decision involves legal and financial nuances well beyond our conversation. That caution, she said, is one of the harder parts of being analytically wired: she can see the shape of the problem clearly but feels the weight of every wrong turn more acutely because of it.

The Turning Point: Planning for Her Own Future Differently

Watching her mother’s care bills arrive each month has changed how Linda thinks about her own retirement — specifically, about what Medicare will and won’t do for her in roughly nine years. She has started reviewing her own Social Security projected benefit statements more carefully. According to SSA’s my Social Security portal, workers can access estimated retirement benefit projections that account for actual earnings history. Linda said the divorce-era gap in her earnings record — combined with years of lower income during the rebuilding phase — has visibly dented her projected monthly benefit.

“I looked at my statement and I could see the divorce years sitting there like a scar,” Linda told me. “Every year I didn’t earn full wages, every year I was in court instead of working at full capacity — it’s all in there.” She is now weighing whether to delay claiming Social Security beyond 67 to allow her benefit to grow, though she is candid that her cash flow situation makes that feel more like a theory than a plan.

The other shift has been accepting that the Medicare she will receive at 65 will have the same gap she is watching swallow her mother’s savings right now. She said she wishes someone had walked her through the distinction between Medicare and long-term care coverage years before it became a live invoice. “Not as advice,” she added quickly, with the careful precision of someone who has learned to hedge. “Just as information. Just so I could have known what I was actually planning for.”

Where Things Stand Now

When I asked Linda what the past fourteen months have looked like in practical terms, she pulled out a small notebook and read me three months of net cash flow figures without commentary. The numbers were tight. Not catastrophic — her income is strong and she is resourceful — but tight in the way that leaves no margin for surprise. Her daughter has two more years at UC Santa Barbara. Her mother’s cognitive decline is slow but consistent. Neither timeline offers a clear exit.

Linda said she does not regret paying for her mother’s care or her daughter’s tuition. Those are not decisions she second-guesses. What she regrets is the years she spent assuming Medicare would be a partner in the former, and that her retirement account balance alone would define her security in the latter. “I built a plan around assumptions that weren’t true,” she said. “That’s on me. I own that. But I also think a lot of people are building the same plan right now and they don’t know it yet.”

She finished her coffee, closed the notebook, and said she had a budget review meeting in twenty minutes. She gathered her things with the composed efficiency of someone who has learned to keep moving even when the numbers are hard. I watched her walk back into the building and thought about the $6,800 invoice arriving again in four days, the way it does every month, and what it costs to love people without enough information to protect them properly.

Related: My Social Security Check Went Up in January — But My Medicare Bill Nearly Wiped Out the Gain

Leave a Reply