Margaret had done everything right. She retired at 66, filed her Medicare paperwork on time, and set up automatic deductions from her Social Security check. Then one afternoon, sorting through a stack of benefit notices, she noticed her Part B premium was nearly $67 a month higher than her neighbor, a woman with nearly identical retirement income. That single moment of curiosity led to a $800 refund and a hard lesson about how Medicare calculates what you owe.

Stories like Margaret’s are more common than most people realize. Medicare Part B premiums are not one-size-fits-all. For millions of enrollees, the monthly amount deducted from Social Security is determined by a surcharge system called IRMAA; the Income-Related Monthly Adjustment Amount. When that system uses the wrong income data, you can end up paying hundreds of dollars more per year than you should.

How Medicare Part B Premiums Are Actually Calculated

The standard 2026 Medicare Part B premium is $185.00 per month, according to Medicare.gov. For most enrollees, single filers earning under $106,000 or married couples filing jointly under $212,000; that’s the number. But for higher earners, IRMAA adds a surcharge on top of that base rate, pushing premiums significantly higher.

Medicare uses a two-year lookback on income, meaning your 2024 tax return determines your 2026 premium tier. Social Security pulls that data directly from the IRS. If your 2024 income placed you in a higher bracket, you’ll pay a higher premium in 2026, even if your income dropped sharply in 2025 or 2026.

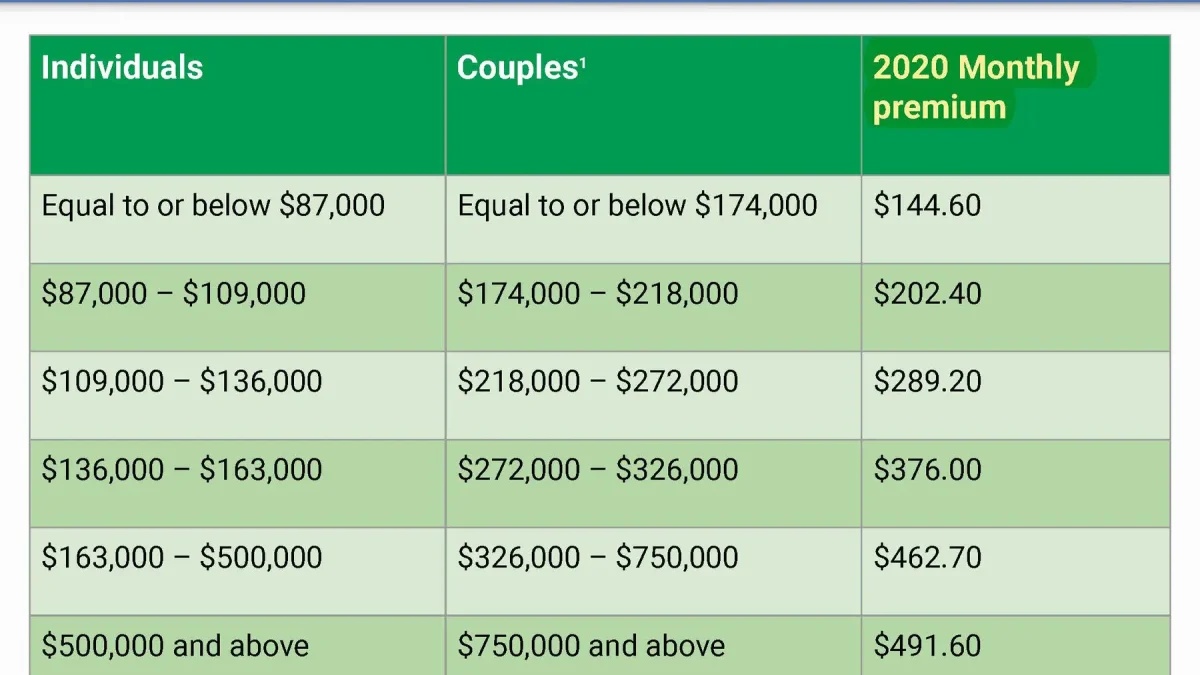

| 2026 Individual Income (2024 Tax Return) | Monthly Part B Premium | Annual Cost |

|---|---|---|

| $106,000 or less | $185.00 | $2,220 |

| $106,001 – $133,000 | $259.00 | $3,108 |

| $133,001 – $167,000 | $370.00 | $4,440 |

| $167,001 – $200,000 | $480.90 | $5,770.80 |

| Above $500,000 | $591.90 | $7,102.80 |

The gap between tiers can exceed $74 per month; roughly $888 per year. That’s not a rounding error. For retirees on fixed incomes, that difference is real money. And the error that triggers it is often something the enrollee never caused: a one-time income spike from a home sale, an inherited IRA distribution, or a severance payment that inflated a single year’s reported income.

Where the Income Calculation Error Comes From

The most common source of IRMAA errors is a mismatch between what the IRS reported to Social Security and what actually reflects your current financial situation. Social Security doesn’t ask you what you earned this year. It looks backward, and that two-year lag creates a structural problem for anyone whose income changed significantly.

Consider a retiree who sold a rental property in 2024, generating a large capital gain that pushed their modified adjusted gross income (MAGI) above $133,000. In 2026, Social Security sees that 2024 income and applies a higher IRMAA tier. But if that person’s 2025 and 2026 income is back below $106,000, they’re paying a surcharge based on income they no longer have.

Errors also occur when the IRS transmits incorrect data. Tax amendments, corrected 1099s, and filing status changes don’t always propagate cleanly to Social Security’s records. If you amended your 2024 return after Social Security pulled your data, your premium calculation may still reflect the original, higher income figure.

How the IRMAA Appeal Process Actually Works

Filing an IRMAA appeal is more straightforward than most people expect. According to the National Council on Aging, you can appeal your IRMAA surcharge due to a life-changing event or an income decrease. Social Security recognizes specific qualifying events that allow you to request a recalculation using more recent income data.

Qualifying life-changing events include:

- Marriage, divorce, or death of a spouse

- Work stoppage or reduction in work hours

- Loss of income-producing property

- Loss of pension income

- Receipt of a settlement from an employer

To file an appeal, you complete SSA Form SSA-44, the Medicare Income-Related Monthly Adjustment Amount; Life-Changing Event form. You submit it to your local Social Security office along with documentation showing your current or projected income. If approved, Social Security recalculates your premium using the more recent income year, and you stop paying the inflated surcharge going forward.

For errors that aren’t tied to a life-changing event; such as a data transmission mistake from the IRS, the process is slightly different. You can call Medicare directly at 1-800-MEDICARE (1-800-633-4227) to flag the discrepancy and request a review. Social Security can also initiate a correction if you provide documentation showing the income figure they used was inaccurate.

“An IRMAA appeal is a petition that you can file with Social Security to reduce your Part B premium if you feel there is a compelling reason why you should not be paying the higher amount.”; Boomer Benefits

What Happens After You File: and What You Can Recover

Once Social Security reviews your appeal and approves a recalculation, your premium adjusts going forward. Refunds for past overpayments are typically credited back to your Social Security benefit, though the timeline varies. Most enrollees see the correction reflected within one to three billing cycles.

The math on recovery is worth understanding clearly. If you were incorrectly placed in the second IRMAA tier, paying $259 instead of $185 per month; that’s a $74 monthly overcharge, or $888 per year. An $800 annual overcharge, like Margaret’s situation, is entirely plausible from a single-tier misclassification. Over two or three years before the error is caught, that compounds quickly.

Here’s a simple way to audit your own situation. Build a quick calculation:

- Find your gross Social Security benefit amount (before deductions)

- Subtract your current Part B premium deduction

- Compare that deduction to the standard rate of $185.00 for 2026

- If the difference exceeds $74, you may be in an IRMAA tier, verify whether that tier matches your actual 2024 income

If you never received an IRMAA determination notice and your single-filer income was under $106,000, you’re almost certainly at the standard rate. But if you did receive a notice; or if your deduction is higher than $185, pull your 2024 tax return and compare your MAGI against the tier thresholds in the table above.

Why This Error Is Surprisingly Easy to Miss

Most Medicare enrollees receive their Part B premium deduction as a line on their Social Security benefit statement. Unless you’re actively comparing that number against published premium tables, an overcharge can run undetected for years. Social Security doesn’t send a separate alert saying “your premium is higher than standard because of IRMAA.” The IRMAA determination notice arrives once, typically in November before the coverage year begins, and many people file it away or discard it without fully understanding its implications.

The two-year lookback compounds the confusion. A retiree who had a high-income year in 2024 due to a one-time event might assume their 2026 premium reflects their current, lower income; not realizing the system is still looking at that older data. By the time they notice, they may have overpaid for 12 or even 24 months.

According to the Elder Law Answers resource on IRMAA appeals, if your income decreases significantly due to certain circumstances, you can request that Social Security recalculate your benefits using more recent income data. That recalculation right exists regardless of whether the original calculation was technically correct, it’s a built-in correction mechanism that most enrollees never use.

The practical takeaway is straightforward: check your Medicare Part B premium deduction annually, compare it against the current year’s published tier thresholds, and verify that the income year Social Security used matches your actual financial situation. A 20-minute review once a year is all it takes to catch an error that could otherwise cost you hundreds of dollars over time.

More Stories Like This

- Everything I Read Said Medicare Had Flexible Enrollment Options — Then a 3-Month Delay Hit Me With a $2,000 Permanent Penalty I Can't Escape (elderlawanswers.com)

- She Missed Medicare Part B by 3 Months — Now She Pays $2,400 Extra, Forever

- thedailycheck.org.org/missed-social-security-payment-by-one-day-1847-lost/” style=”color:#0284c7;text-decoration:none;font-weight:500″>Missing Your Social Security Payment Date by Even One Day Can Permanently Erase Benefits — Here Is the $1,847 Rule Nobody Tells You About

Frequently Asked Questions

Leave a Reply