Open enrollment ends, your Medicare card arrives, and then January’s bank statement shows a number you don’t recognize. For millions of beneficiaries, that moment arrives without warning, a Part B premium that’s $42, $68, or even $170 higher than the standard rate, with no explanation letter that makes any sense. If you’ve been on hold with CMS and still don’t have a straight answer, there’s a strong chance IRMAA is the reason.

IRMAA; the Income-Related Monthly Adjustment Amount, is a surcharge added to your Medicare Part B and Part D premiums when your income crosses certain thresholds. As of March 2026, nearly six million seniors owe these extra charges, according to reporting from The Wall Street Journal, according to wsj.com. Most of them had no idea the rule existed until they saw the bill.

What Is IRMAA and Why Did Nobody Tell You About It?

IRMAA stands for Income-Related Monthly Adjustment Amount. It is an extra charge applied to Medicare Part B and Part D premiums for people whose income exceeds a set limit. According to the National Council on Aging, IRMAA is a higher rate that some higher earners may have to pay; and it is paid in addition to your standard monthly premium, not instead of it.

The standard Medicare Part B premium has climbed steadily. In one recent year, it jumped $21.60 to reach $170.10 per month. Add an IRMAA surcharge on top of that, and a retiree at the first income bracket above the standard threshold can suddenly owe $244.60 or more. At higher income tiers, the number climbs further.

CMS doesn’t proactively call you to explain this. Social Security sends a notice, but it often arrives buried in a stack of other Medicare correspondence, and the language is dense enough that many people assume it’s a form letter rather than an actionable bill change.

The IRMAA Income Brackets: What the Thresholds Actually Look Like

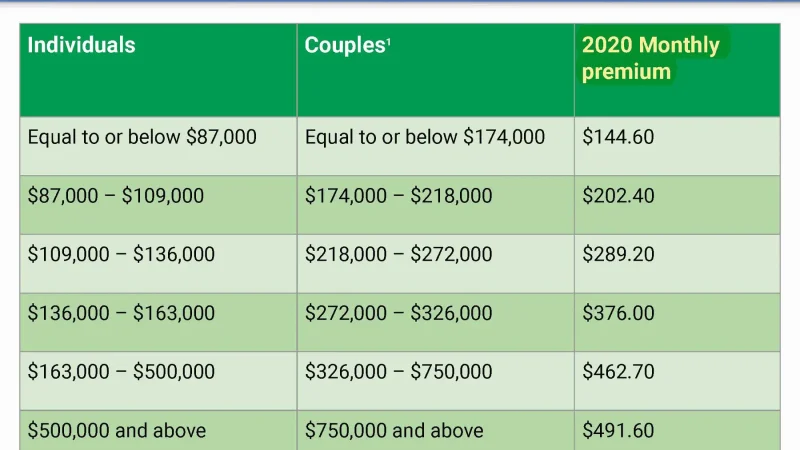

IRMAA uses a two-year lookback rule. Your 2026 premium is based on your 2024 tax return. If your income crossed a threshold in 2024; even once, due to a home sale, a Roth conversion, or a required minimum distribution, you may be paying a surcharge in 2026 that feels completely disconnected from your current financial situation.

| 2024 Individual MAGI | 2024 Joint MAGI | 2026 Monthly Part B Premium | IRMAA Surcharge Added |

|---|---|---|---|

| Up to $103,000 | Up to $206,000 | Standard rate | $0 |

| $103,001–$129,000 | $206,001–$258,000 | Approximately $244–$248 | ~$69–$74/month |

| $129,001–$161,000 | $258,001–$322,000 | Approximately $349–$355 | ~$174–$180/month |

| $161,001–$193,000 | $322,001–$386,000 | Approximately $454–$462 | ~$279–$287/month |

| Above $500,000 | Above $750,000 | Approximately $594+ | ~$419+/month |

Note: Exact 2026 bracket figures are subject to annual CMS adjustments. Check CMS, according to cms.gov.gov for the current year’s official thresholds. The figures above reflect approximate ranges based on recent historical adjustment patterns.

Does “Medicare Income Limits” Mean the Same Thing as IRMAA?

Not exactly; though the terms are closely related and often used interchangeably in conversation. “Medicare income limits” is a broad phrase that can refer to several different programs: IRMAA surcharges for higher earners, Medicare Savings Programs for lower-income beneficiaries, or Extra Help eligibility for Part D costs.

IRMAA is specifically the mechanism that raises your premium above the standard rate. Medicare Savings Programs do the opposite, they help lower-income beneficiaries pay premiums, deductibles, and copays. So when someone says “my premium changed because of income limits,” they might mean IRMAA (premium went up) or they might mean a savings program adjustment (premium went down).

For most people whose premiums jumped unexpectedly, IRMAA is the culprit. The confusion is understandable because Social Security administers IRMAA determinations while CMS administers the actual Medicare program; meaning calls to CMS often result in representatives who can explain the billing but not the income-based calculation behind it.

How the IRMAA Lookback Rule Catches People Off Guard

This is where the $42 jump becomes explainable. Say you retired in 2024 and took a large Roth IRA conversion to reduce future RMDs. That single financial move may have pushed your Modified Adjusted Gross Income (MAGI) above the first IRMAA threshold, even if your ongoing retirement income is well below it. Two years later, in 2026, you’re paying a higher Part B premium based on that one-time spike.

The same thing happens with home sales. Selling a home with significant appreciation can generate a capital gain large enough to cross an IRMAA bracket, even after the $250,000 individual exclusion. Beneficiaries who sold property in 2024 and didn’t account for Medicare implications may now be seeing the result on their 2026 statements.

Required minimum distributions are another trigger. As account balances grow and RMD rules require larger withdrawals, more retirees find themselves crossing IRMAA thresholds they never anticipated. According to Baird Wealth Management, Medicare premiums can rise with income due to IRMAA in ways that aren’t obvious until the bill arrives.

Why the $42 Jump Is Important: and What You Can Do About It

A $42 monthly increase is $504 per year. At the second IRMAA bracket, the annual surcharge exceeds $2,000. For a couple, both on Medicare, those numbers double. Over a five-year retirement window, IRMAA costs can represent a meaningful and entirely unplanned expense; one that compounds if income doesn’t drop back below the threshold.

Three actions are worth taking immediately if you’ve received an unexpected premium increase:

- Request your IRMAA determination letter from Social Security. This document specifies which tax year was used and what income figure triggered the surcharge. If you don’t have it, call SSA at 1-800-772-1213.

- File a Life-Changing Event appeal if your income has dropped. According to Boomer Benefits, an IRMAA appeal is a petition you can file with Social Security to reduce your Part B premium if there is a compelling reason — such as retirement, divorce, or the death of a spouse — why your current income is lower than the year used for the determination. Use SSA Form SSA-44.

- Plan future income events with IRMAA thresholds in mind. If you’re considering a Roth conversion, asset sale, or large distribution, run the numbers against current IRMAA brackets before executing. Staying $1 below a threshold can save hundreds of dollars annually.

IRMAA appeals based on life-changing events have a reasonable success rate when the income reduction is documented and genuine. Retirement itself qualifies as a life-changing event — meaning if you retired in 2025 and your income dropped significantly, you may be able to appeal a 2026 surcharge based on projected 2025 or 2026 income rather than your higher 2024 earnings.

What This Means for Your Retirement Budget Going Forward

Medicare Part B costs are not fixed. They shift annually based on CMS adjustments and shift again based on your income from two years prior. A retirement budget that treats Part B as a flat line item is almost certainly wrong for anyone with variable income, investment accounts, or real estate.

Financial planners who specialize in retirement income increasingly treat IRMAA planning as a core service — not an afterthought. Decisions about when to take Social Security, how to sequence Roth conversions, and how to manage RMDs all carry Medicare premium implications that can be quantified and, in many cases, managed.

If your premium jumped and nobody at CMS could explain it clearly, that’s a systemic communication failure — not your fault. IRMAA is a legitimate policy with real income thresholds and real appeal rights. Knowing those rights, and the two-year lookback rule behind them, is the difference between paying a surcharge indefinitely and potentially getting it reduced or eliminated.

Frequently Asked Questions

Leave a Reply