Roughly 1 in 4 American workers will experience a disabling condition before they reach retirement age, according to data tracked by SSA.gov Disability Benefits. That statistic is easy to read and move past — until you’re sitting in a plastic chair next to the person it describes.

I was at the Social Security Administration field office on Arden Way in Sacramento last February, working on a piece about delayed SSDI processing times, when a man in a faded gray jacket sat down beside me in the waiting room. He had a manila folder on his lap, thick with papers, and he kept smoothing the cover with his thumb the way people do when they’re nervous but trying not to show it. That was Travis Dupree.

Travis is 48 years old. He spent most of his adult life as an insurance claims adjuster — the person on the other end of the phone when things go wrong for other people. Then things went wrong for him.

The Call That Changed Everything

Travis told me he started noticing the symptoms in the spring of 2023 — persistent fatigue, nerve pain in both hands that made typing nearly impossible, and a series of small but accumulating errors at work that his manager began flagging. By August of that year, his neurologist had a diagnosis: an advanced degenerative disc condition compounded by nerve damage in his cervical spine. He was placed on short-term disability through his employer almost immediately.

“I thought it would be a few months,” Travis told me, leaning forward with his elbows on his knees. “I’d handled disability claims for fifteen years. I knew how the system was supposed to work. I thought I knew.”

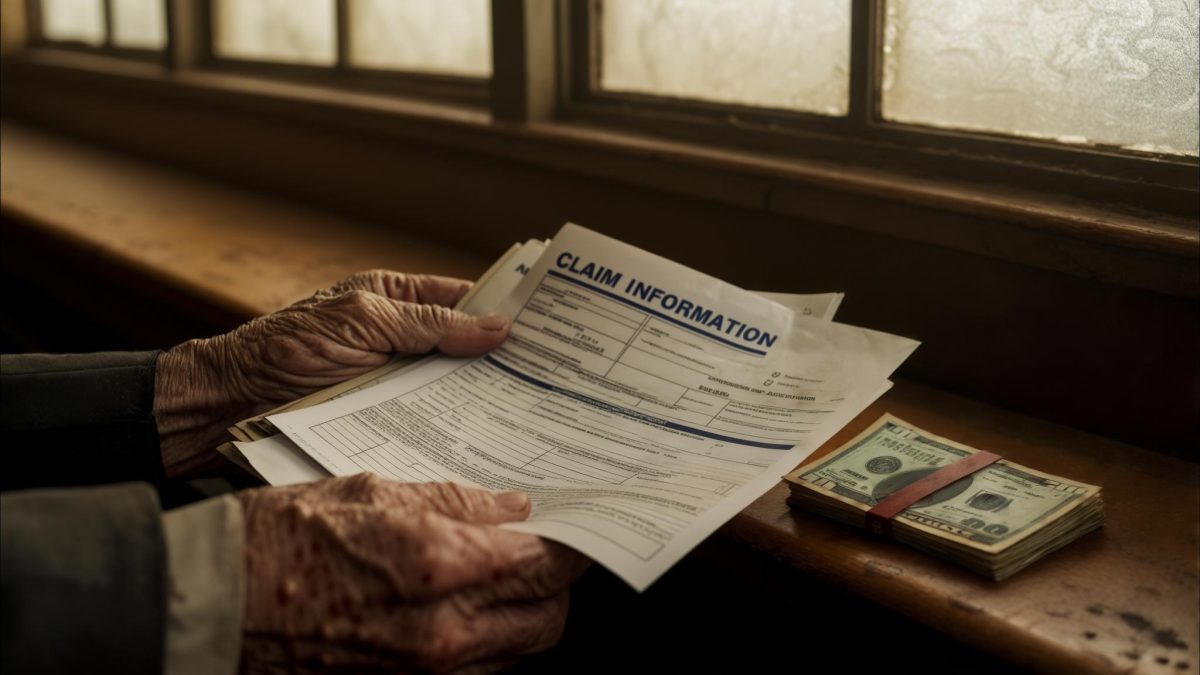

His employer’s short-term disability ran out after six months. He filed for Social Security Disability Insurance in February 2024. What followed was an 11-month wait — longer than the national average, he noted, which he knew because, again, he used to work in claims.

His application was approved in January 2025. His monthly benefit was set at $1,340 — a figure calculated from his earnings record, which reflected years of a modest but steady income as a mid-level adjuster. Under SSA.gov Retirement Benefits guidelines, disability benefit amounts are tied to a worker’s lifetime earnings history, meaning lower-income earners receive lower monthly payments even when their need is greatest.

When COBRA Costs More Than the Rent Check

The number that stopped me cold when Travis said it out loud: $1,850 per month for COBRA continuation coverage. His family — Travis, his wife Marlena, and their two kids, Jaylen (7) and Destiny (6) — needed health insurance. Travis’s ongoing treatment for his spine condition isn’t optional. Marlena’s part-time retail job doesn’t include benefits.

Their rent on a two-bedroom apartment in a quieter part of Sacramento’s Arden-Arcade neighborhood is $1,595 per month. The COBRA bill exceeds it by $255 every single month.

The household math is brutal. Travis brings in $1,340 in SSDI. Marlena clears approximately $1,100 a month after taxes from her part-time hours at a home goods store. That’s $2,440 combined. After the COBRA premium, they have $590 left for everything else. Rent alone consumes nearly three times that amount. Travis told me they’ve been drawing down the last of a small savings account — roughly $4,200 as of February — to bridge the gap each month.

No Retirement Savings at 48 — and the COLA That Barely Moved the Needle

Travis has no retirement savings. Not a depleted account — none at all. During the years he was building his career, there were car repairs, a period of unemployment in 2017, and what he described as “just always something.” He never opened an IRA. His employer offered a 401(k) but he never enrolled at a contribution level that stuck.

When the Social Security Administration announced a 2.5% Cost-of-Living Adjustment for 2025, as documented on SSA.gov COLA Information, Travis did the math immediately. A 2.5% increase on a $1,340 benefit works out to $33.50 per month. His COBRA premium, by contrast, had increased by $74 at the same time due to his former employer’s annual insurance rate adjustment.

“The COLA went up thirty-something dollars,” he told me flatly. “The insurance went up seventy-four. I’m going backwards.”

Travis understood this with the precision of someone who spent his career reading policy documents. The COLA is designed to track inflation broadly, not the inflation experienced by people whose largest expense is a health insurance premium. For him, it was an adjustment that moved in the right direction — and still left him further behind.

The Texture of Generosity Under Pressure

The detail about Travis that stayed with me longest wasn’t financial. It was something his wife Marlena mentioned when I followed up by phone a few weeks after meeting Travis in that waiting room. She said that when their neighbor — a single mother two doors down — mentioned she couldn’t afford new shoes for her son before school started, Travis had quietly ordered a pair online and left them at her door. This was in September, when their savings account had already dropped below $6,000.

When I mentioned this to Travis, he was quiet for a moment. “Her kid needed shoes,” he said. “What was I going to do, not get them?”

Travis told me that Jaylen, his seven-year-old, had recently asked why they don’t go to Legoland anymore. They went twice, years ago, before the diagnosis. Travis told him they were “saving up for something better.” He didn’t know what that something was, but it was what came out.

Where Things Stand Now

When I last spoke with Travis in late March 2026, the savings account was down to approximately $1,400. He had submitted paperwork to explore Medicaid eligibility for the kids and had spoken with a benefits counselor through a local nonprofit about the possibility of transitioning off COBRA. He was also in the early stages of understanding what his SSDI payments might look like if his condition never improves enough to return to work — a scenario the SSA’s disability program provides for, but one that comes with its own complex rules around work attempts, continuing disability reviews, and eventual Medicare eligibility after a 24-month waiting period.

That Medicare eligibility date — January 2027 — has become something Travis circles in his mind like a fixed point on a map. It won’t solve everything. But it would replace the $1,850 COBRA bill with Medicare premiums that, for most SSDI recipients, run significantly lower. He knows this. He’s counting the months.

“I know the rules better than most people,” he told me. “I just never thought I’d be the one they applied to.”

I left that conversation thinking about the gap between knowing a system and being inside it. Travis Dupree spent fifteen years understanding exactly how disability insurance works. He could probably explain SSDI’s five-step evaluation process in his sleep. None of that knowledge added a single dollar to his monthly check or subtracted one from his COBRA bill. It just meant he understood, with unusual clarity, how close to the edge he was standing.

His folder is still thick with papers. He’s still smoothing the cover with his thumb.

This article reflects reporting conducted in February and March 2026. This story is not financial advice. If you are navigating disability benefits or insurance coverage decisions, please consult a licensed benefits counselor or contact the SSA directly at 1-800-772-1213.

Leave a Reply