Roughly 1 in 3 American workers have no retirement savings at all, according to estimates from financial research organizations — but for those who lost years of earned income during the COVID pandemic, the Social Security picture is often worse than they realize. When I sat down with Carlos Mendez, 55, at a corner table of a Doral restaurant on a Tuesday afternoon in late March, he was on his lunch break. He ordered water. He told me he’d eaten before he came.

That detail said everything about the man before he said a single word.

A Career Built Over Decades, Erased in 14 Months

Carlos Mendez had managed restaurants in Miami-Dade County for nearly three decades before the pandemic shuttered his employer’s location in April 2020. He wasn’t laid off immediately — he held on, managing skeleton crew operations, then takeout-only shifts — but by June 2020, the doors closed for good. He spent the next 14 months burning through the savings he and his wife had carefully built.

“We had about $34,000 put away,” Carlos told me, leaning forward with his hands folded on the table. “That was our cushion. By August of 2021, it was gone. Every dollar of it. Between the mortgage, the kids, groceries — it just disappeared.”

Carlos and his wife have four children between them: two biological sons of his, ages 14 and 11, and two daughters from his wife’s previous relationship, ages 16 and 9. Her ex-husband pays child support — when he feels like it, Carlos said, with a short, humorless laugh. “Some months it comes. Some months we text and text and nothing. We’ve stopped counting on it.”

He found new work in late 2021, managing a regional chain location in Doral. The pay is steady but lower — roughly $52,000 a year compared to the $68,000 he earned before. At 55, with four kids still at home and zero in savings, retirement feels both urgent and impossibly far away.

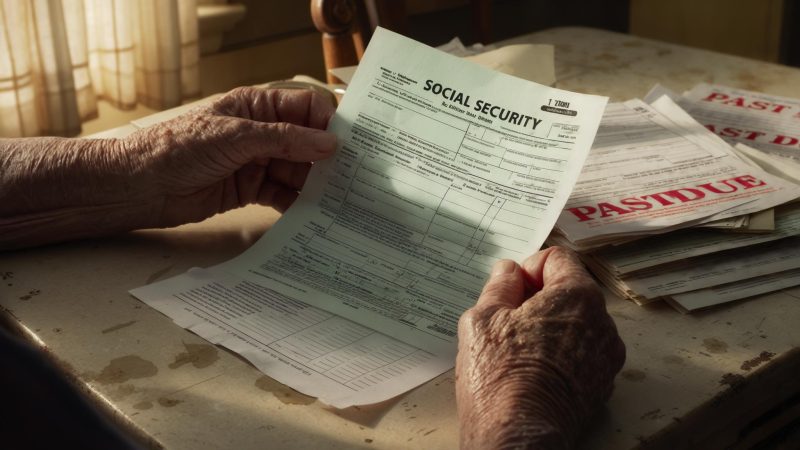

The Moment He Logged Into the SSA Portal

The turning point in Carlos’s story — the moment that brought him to my attention after a mutual contact suggested I speak with him — came last November. His wife had read something online about the my Social Security portal, a free tool where workers can review their full earnings history and see projected benefit amounts at different retirement ages.

Carlos had never logged in before. He’d assumed, vaguely, that he’d eventually collect something reasonable. He’d paid into the system his entire working life. “I figured it would be okay,” he said. “I never actually looked.”

What he saw shook him. His earnings record showed two years — 2020 and a portion of 2021 — with sharply reduced income. Because Social Security retirement benefits are calculated based on a worker’s highest 35 years of indexed earnings, according to the SSA’s benefit calculation page, those low-income years weren’t going to be dropped from the equation the way he’d hoped. He didn’t have 35 strong years to override them yet.

“The number they showed me was a lot lower than I expected,” Carlos said. “I don’t want to say the exact number because it’s embarrassing, honestly. But I’ll tell you — it was not enough to live on. Not even close.”

Understanding the COLA — and Why It Barely Registered for Carlos

The Social Security Administration announced a 2.5% Cost-of-Living Adjustment for 2025, effective with January 2025 benefit payments. For the average recipient collecting $1,927 per month in late 2024, that translated to roughly an additional $48 per month. The 2025 COLA followed a 3.2% increase in 2024 and an 8.7% surge in 2023 — the largest in four decades — driven by post-pandemic inflation.

For current retirees, those adjustments matter. But Carlos isn’t collecting yet. He’s 55. His full retirement age, for someone born in 1971 according to SSA’s retirement age chart, is 67. That’s 12 years away. The COLA he hears about on the news — the one that gave retirees a modest bump in January — means almost nothing to him right now.

“Everybody keeps talking about COLA this and COLA that,” Carlos said, a slight edge in his voice. “But I’m not there yet. I’m still just trying to make the mortgage and keep the lights on. Those people getting those checks — I’m happy for them. That’s just not my world right now.”

What his world looks like: a household of six running on one steady income, supplemented by his wife’s part-time work as a medical biller and the unpredictable arrival of child support from her ex. Some months they’re fine. Some months Carlos goes without lunch.

The Real Cost of the Work Gap — by the Numbers

I asked Carlos if he’d done any math on what those COVID years might cost him in retirement. He had — with help from a calculator tool on the SSA website. The rough estimate he walked me through was sobering.

These figures are Carlos’s estimates using the SSA’s own online tools — not official projections, and they will shift as he continues working and earning. But they illustrated something he hadn’t fully grasped before that November evening in front of his laptop: the compounding cost of a single crisis, playing out over a 20-year retirement horizon.

The Man Behind the Numbers

I asked Carlos about his four kids. He lit up in a way that he hadn’t during the financial conversation. His 16-year-old stepdaughter wants to study nursing. His 14-year-old son is obsessed with video game design. He talked about each of them with a specificity and warmth that made it clear they were not abstractions to him — they were the entire point.

“People ask me how I manage with four kids and this income and everything,” he said. “I don’t think about it that way. I think about what each of them needs that week. You just do it. You figure it out.” He paused. “The problem is I’ve been figuring it out for so long that I forgot to figure out what happens to me at the end.”

Carlos has 12 years before he reaches full retirement age. He told me his plan — as much as there is one — is to keep working, keep paying into Social Security, and hope the higher-earning years ahead replace some of the COVID-era zeros on his record. He knows the math will improve the longer he works. He’s just not sure life will cooperate long enough to let it.

His wife’s ex missed three payments in the last four months. The oldest daughter needs braces. His restaurant reduced management hours twice in the past year citing “operational adjustments.” Every time he gets close to stable, he said, something shifts beneath his feet.

“I’m not asking for sympathy,” Carlos told me as his break neared its end. “I’m 55. I’ve seen harder things. I just want people to know — you can do everything right, work your whole life, and still end up looking at a number on a screen that scares you. That can happen. It happened to me.”

He left a $4 tip on his water glass. I watched him walk back across the parking lot in the March heat, already reaching for his phone before he pushed through the door.

Related: My Social Security Check Went Up in January — But My Medicare Bill Nearly Wiped Out the Gain

Leave a Reply