The letter arrived on a Tuesday in late January 2026, wedged between a water bill and a grocery store circular. Doris Bianchi, 65, a security guard who works overnight shifts at a distribution warehouse on the south side of Louisville, set it on her kitchen counter for two days before she opened it. She already knew what it was. She had been waiting for it for months.

I first heard about Doris from Pastor Gerald Whitmore at Cornerstone Fellowship Church in the Shawnee neighborhood of Louisville. He reached out after I published a piece on Social Security payment delays and mentioned he knew a woman in his congregation whose situation was more complicated than most. When I called Doris to introduce myself, she was quiet for a moment before saying, “I don’t really talk about money with people. But I’m tired of carrying this alone.”

A Budget Built on Two Unpredictable Numbers

When I sat down with Doris at a corner table in a diner near her apartment in the Russell neighborhood, she spread out two envelopes and a worn spiral notebook. The notebook had columns of numbers going back to mid-2023, when she first started drawing Social Security benefits at age 63 — a decision she made early because her work hours had started shrinking.

Doris receives $1,180 per month in Social Security retirement benefits. Because she filed before her full retirement age of 67, her benefit was permanently reduced from what she would have received had she waited. Her birthday falls on the 11th of the month, which means — under the SSA’s payment schedule — her check arrives on the second Wednesday of every month. In April 2026, that date was April 8.

On top of her Social Security, Doris works security shifts that vary widely. Some weeks she logs 38 hours at $15.20 per hour. Other weeks, when staffing runs over or a contract site goes dark, she is called in for only 12 or 14 hours. “I’ve had months where I brought home $2,400 between everything,” she told me. “And I’ve had months where it was barely $1,500. You cannot plan a life on that.”

The instability is not new. Doris went through a difficult divorce in 2017 that left her responsible for joint debts her former spouse had stopped paying. One of those — a medical bill from a 2014 emergency room visit — was sold to a collections agency and had accrued interest and fees over roughly 11 years to reach approximately $6,400.

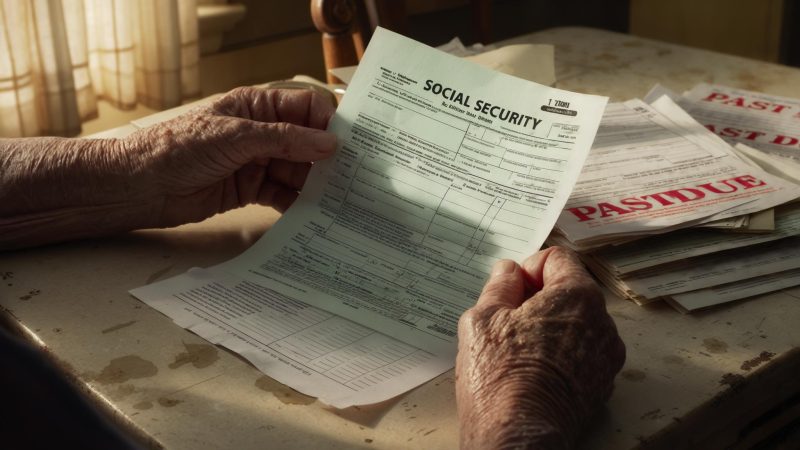

What the Letter Actually Said

The January letter was from a debt collections firm based in Ohio. It stated that the firm had obtained a civil judgment in Kentucky court and intended to pursue garnishment of Doris’s wages and “any applicable income streams.” Doris read that phrase — “any applicable income streams” — as a direct threat to her Social Security deposit.

What Doris did not know — and what took her several weeks and a visit to a legal aid office to understand — was that Social Security benefits carry significant federal protections against garnishment by private creditors. Under federal law, ordinary consumer debt collectors and civil judgment holders generally cannot garnish Social Security income directly from the SSA or from a bank account where Social Security is the sole deposit.

The protection is not absolute, though. As the SSA explains on its official benefits page, Social Security can be garnished for specific federal obligations, including unpaid federal taxes, defaulted federal student loans, and court-ordered child support or alimony. Doris’s debt was a private civil judgment — not a federal obligation — which placed it in a different category entirely.

The Part That Still Hurt

Here is where Doris’s story becomes more complicated than a straightforward win. Her Social Security check was protected. But her security guard wages were not.

Under Kentucky law, a creditor with a valid court judgment can garnish up to 25% of a worker’s disposable earnings — or the amount by which weekly earnings exceed 30 times the federal minimum wage, whichever is less. For Doris, in a week where she brings home $380 in take-home pay, that could mean roughly $65 to $95 removed before she ever sees it.

“They told me my Social Security was safe,” Doris said when I asked her how she processed the legal aid visit. “And I cried. I actually cried in that little office. And then they told me about my paycheck and I stopped crying pretty fast.”

The wage garnishment began in February 2026. In a week where Doris worked 32 hours, approximately $88 was withheld from her check. In a lighter week of 18 hours, the garnishment amount dropped to roughly $40. The inconsistency added a new layer of unpredictability to a budget already stretched thin.

How the 2025 COLA Fit Into the Picture

One thing that arrived on the same timeline as the debt letter — and that Doris had been tracking closely — was the 2025 Cost-of-Living Adjustment. The SSA announced a 2.5% COLA for 2025, which took effect with January 2025 benefit payments. For Doris, that adjustment added approximately $28 per month to her Social Security deposit, bringing her from roughly $1,152 to $1,180.

Twenty-eight dollars a month. Doris almost laughed when she said it out loud. “The government gives me twenty-eight dollars more and the debt people take eighty. I’m going backward, but at least I know my Social Security is mine.”

There was something in that sentence — “at least I know my Social Security is mine” — that carried more weight than she probably intended. For Doris, the Social Security check arriving on the second Wednesday of each month had become her single fixed point. Her work schedule shifted, her take-home pay fluctuated, and now her wages had a lien on them. But that one deposit, on that one predictable day, was hers.

Where Things Stand Now

When I last spoke with Doris in late March 2026, she had been under the wage garnishment for roughly six weeks. The debt firm estimated that at the current rate, the balance would be paid off in approximately 19 to 24 months — assuming her hours stayed consistent, which they have not always done.

She has also started attending a financial literacy group that Pastor Whitmore runs at Cornerstone on Thursday evenings. She goes, she told me, more for the company than the curriculum. “I’m not twenty-five. I know what a budget is. What I need is to not feel ashamed about where I ended up.”

There is a realism to Doris that I found striking — not bitterness exactly, though she acknowledged she carries some, but a clear-eyed accounting of how things went wrong and a stubborn refusal to let that be the final word. She is still working overnight shifts. She is still watching for that second-Wednesday deposit. She is still counting weeks until the garnishment ends.

When I left the diner that afternoon, Doris was still sitting at the table, the spiral notebook open in front of her, writing down numbers. She waved without looking up. The story she is writing with those numbers is not finished yet.

Related: A $23,400 Debt Was Chasing His Social Security Check — Until Diego Underwood Found This Federal Rule

Leave a Reply